Assortment of market factors have combined to push muni rates to investor-friendly levels

Is this a once-in-a-lifetime moment for municipal bonds? There is no unequivocal answer, but it could be one of those periods that investors will look back on and say “wow, I should have looked past the market volatility and built up some exposure in the muni space.”

In addition to higher interest rates across the fixed income universe, a variety of factors have pushed taxable equivalent yields on munis higher, to the point of generating equity-like returns in some instances.

The ride hasn’t been comfortable since early 2022 for this market, but the road ahead appears promising. And for those who lock in rates now, that smooth ride could extend for years.

The Macro Backdrop to Rising Yields

Although Federal Reserve policymakers have largely been espousing the party line of “higher for longer” since August 2022, the bond markets seemed caught off guard by the recent confirmation of this stance at this September’s FOMC meeting. Or perhaps it’s a heightened awareness of the magnitude of US Treasury supply and diminished role of central bank buyers. Either way, the ensuing selloff led to a nearly -4.00% return for the third quarter, according to ICE BofA US Municipal Securities Index.

Added Factors to Muni Yields’ Rise

Municipal bond market’s activity against this backdrop is best described as “disorderly”. The muni market is fragmented to begin with and not always the most efficient or transparent, but when large spikes in trading volume and volatility are taking place, muni bonds can have sharp reactions, as evidenced by the nearly 3.00% decline in September—its worst monthly performance since September 2022.

Yes, the broad rise in yields was a factor in the dreary results, but some of the unique characteristics of the muni market enhanced the downdraft to drive yields to very attractive levels.

Seasonality

Muni bond market activity frequently follows some historical trends. Prices tend to sag (resulting in higher yields) during spring months as individuals sell holdings to cover tax liabilities, but they generally rebound during the summer months amid a wave of bond redemptions and coupon payments. The midyear rollover.

September, October and into November generally feature declines due to two reasons:

-

It’s traditionally a period with few redemptions and limited coupon payments, so there are less proceeds to be reinvested.

-

The new issue supply tends to surge as states and municipalities push for financing on projects that may have been delayed during the summer but need to move forward before holiday season and year-end.

Tax-loss Harvesting Back in Vogue

For several years prior to 2022 there were few opportunities to sell bonds with losses in market value in order to offset other asset gains, given that during that time bonds generally stayed steady or increased in value.

Recent losses haven’t reached the degree that we saw in 2022, and yields are starting from a much higher point than they did last year. But it’s the fourth quarter, so tax loss harvesting is being revisited, and the opportunity to book losses further pressures muni prices.

If I Wait Just One More Day …

Aside from the surging new supply, bond fund managers who have to sell to meet redemptions, tax-minded investors harvesting losses, and a general trend toward higher rates for longer, tepid demand is keeping muni yields high.

Yes, reduced demand is par for the course in a market more focused on selling, but perhaps exacerbating the wait-and-see mindset are money market yields around 5%. While such accounts offered virtually no competition for investors’ cash when they featured miniscule returns, sitting in cash is no longer a borderline punitive choice.

The Silver Lining

At times such as this, we know what many investors are thinking: Conditions are so challenging, we should wait for things to settle down. Once the market stabilizes, then we’ll start to venture back in.

We get it. The market is volatile, and it doesn’t feel like a good time to participate. There have been similar situations in the past. Times when it felt like things would only get worse but stabilized or even snapped back and the opportunity passed.

No one knows what will become of muni yields in the coming months, quarters, and years, and we certainly could see them climb higher.

But with taxable equivalent yields on high-quality bonds in the 6.00% to 7.00% and higher range, we contend it’s worth considering. Perhaps in the short-term we’ll see continued volatility, but locking in these yields may be fulfilling in six months, 18 months, or five years from now.

Quality Concerns Limited as Well

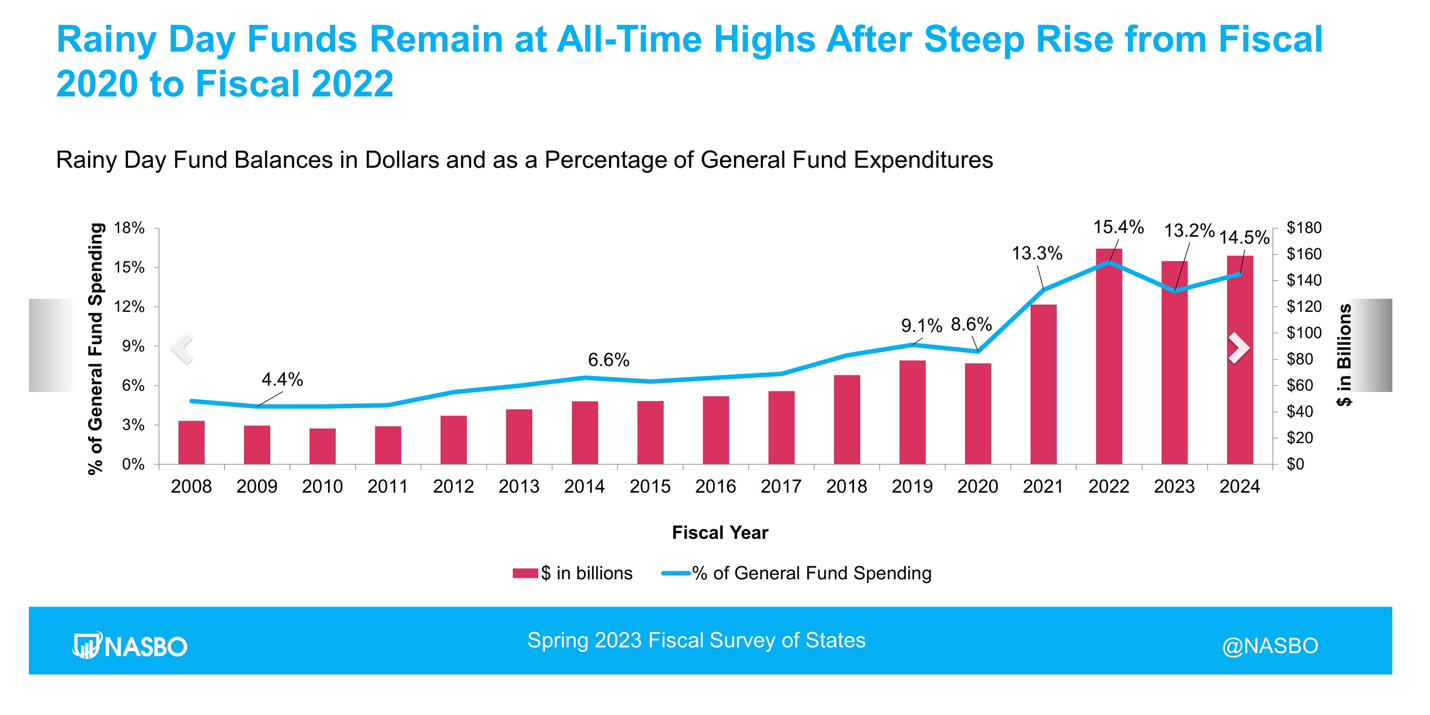

Plus, the creditworthiness of many muni bond issuers is currently exceptional—bolstered in part by state rainy day funds hovering near all-time highs in 37 states. As tax revenues didn’t decline meaningfully during the pandemic, cities and states received an enormous amount of federal aid and stimulus money, and current tax revenues in many locations are surpassing pre-Covid levels, it’s generally a very positive credit environment.

Source: https://www.nasbo.org/reports-data/fiscal-survey-of-states

Source: https://www.nasbo.org/reports-data/fiscal-survey-of-states

We will continue to avoid project-specific types of credits such as those tied to nursing homes, convention centers, and small liberal arts colleges. However, state and local issuers also have a number of levers to pull in the event of an economic slowdown or recession.

How We’ve Been Responding

As we survey the current environment, we are committed to our investment principles. There’s no reason to be reaching for yield on mediocre credits given the ample supply of quality bonds trading at compelling prices.

From a tactical standpoint, we are finding attractive yields across the muni yield curve, a relatively rare occurrence that has prompted a recommendation to invest in short-, intermediate-, and long-term bonds if they meet an investor’s goals and risk tolerances.

And yes, where it’s beneficial, we’re recommending sales to harvest some tax losses, as we’re confident that the positions being exited can be replaced by high-quality issues offering healthy yields.

We know today’s muni market landscape appears treacherous and the coming months could continue to be choppy, but for investors with a long-term horizon, it has the potential to be rewarding.